{kind=link}

Advertised vehicle inventory in the US soared to 3.056 million

units in September 2024—marking a significant 4.7% increase

from the previous month and breaking the three-million mark for the

first time in our dataset. This surge aligns with a broader trend

we've observed over the past two years, where inventory levels

consistently rise in the fall.

The vehicle inventory rise appears across most OEMs and

segments, with some exceptions. Stellantis brands are down vs. last

month (Jeep -4.1%, RAM -1.4%, Dodge -9.1%) and a couple of premium

brands have decreased as well (Audi -7.8%, Cadillac -1.6%, Lincoln

-0.8%)

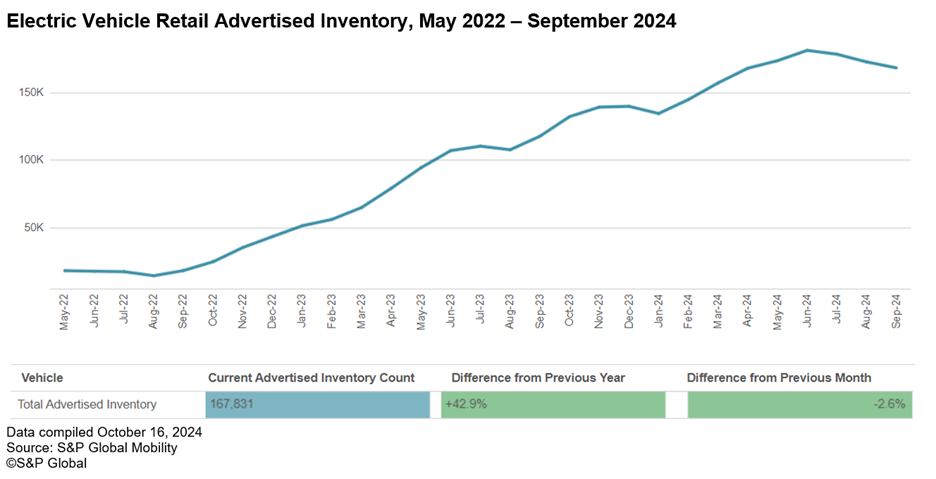

Interestingly, while overall inventory has been growing,

electric vehicle inventory has decreased and is down 2.6% vs.

August. This has reversed a trend that we had seen in previous

months where EV inventory was growing more than the industry as a

whole.

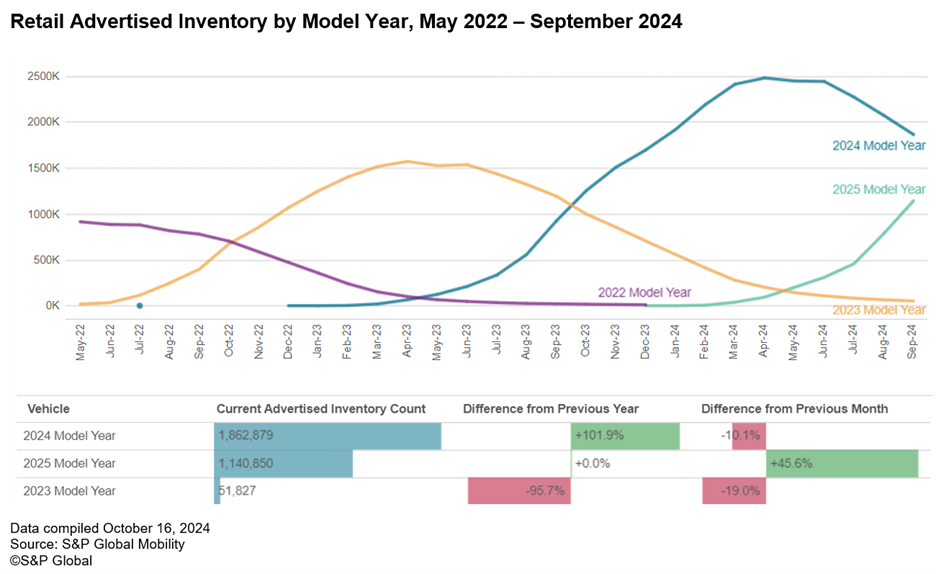

The model year detail helps to explain much of the overall

industry-level results. The roll-out of the 2025 model year

continues to accelerate and is up 45.6% vs. the end of August.

Meanwhile, 2024 and 2023 model year inventories have decreased by

10.1% and 19.0%, respectively.

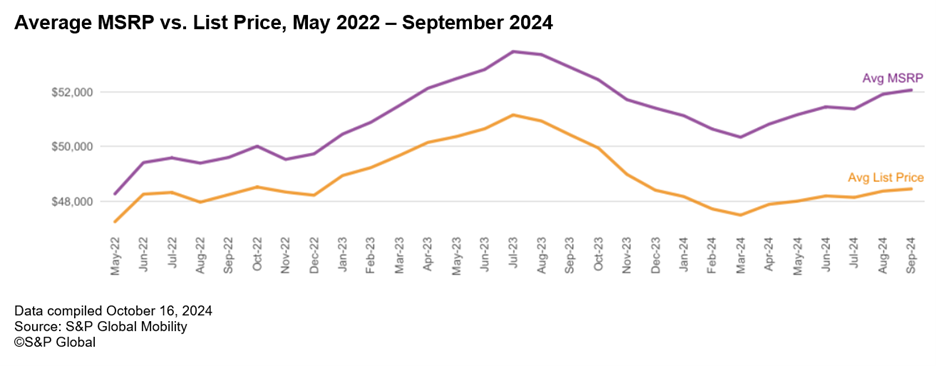

Prices also continue to rise, with the average MSRP standing at

$52,066 at the end of September, up 3.3% compared to March 2024.

The average dealer list price has increased to $48,460, an increase

of 2% vs. March.

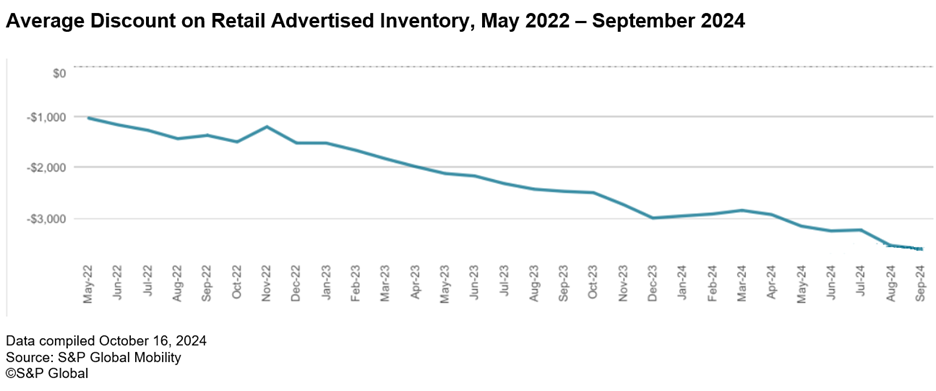

This gap can be seen through

This gap can be seen through

the increase in the average listed discount, which has reached

$3,606 at the end of September. This is an increase of 21.2% since

March.

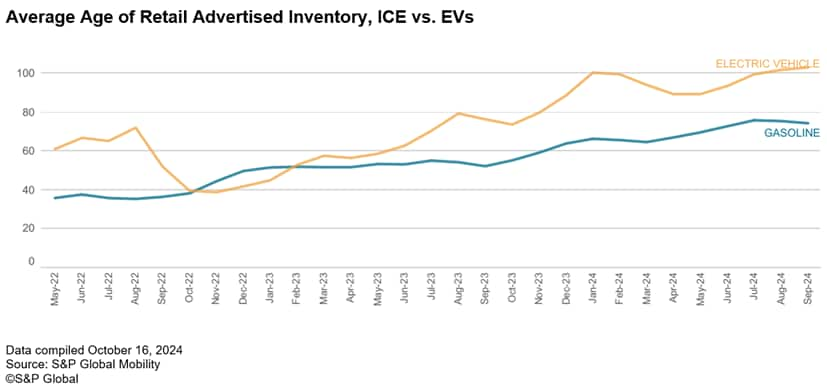

The average age of advertised inventory decreased slightly to 79

days in September but is up from 56 days last September. In the

following chart, we can see that gasoline vehicles have been

advertised for 74 days on average, while electric vehicles are

aging at a greater rate and now have been listed for 103 days on

average.